There are a number of ways in which you can set up and run your business in the UK. In this guide created by OrangeGenie, we look at the differences between sole trader, partnership, Ltd and PLC. We will focus on explaining what the type of company is, the tax implications, and the advantages and disadvantages of each.

What is a Sole Trader?

What is a Sole Trader?

A sole trader is someone that sets up and owns their own business; they reap the rewards and benefits but also have unlimited liability. Unlimited liability means that the sole trader is personally responsible for all of the businesses liabilities and losses.

How to set up a Sole Trader business?

The set-up of a sole trader business is the easiest, cheapest and simplest method out of all of the business structures available. You would need to register your sole trader business with HMRC by the 5th October in your business’s second tax year of trading, if you don’t you could be fined.

In terms of choosing a name for your business, you can use your personal name, or alternatively, you can choose a business name. However, you need to be aware that a sole trader name cannot include the following:

- Ltd, Limited, Limited Liability Partnership, PLC or Public Limited Company

- Offensive language

- An existing trademark

HMRC have a list of sensitive words and expressions that you would need to take into consideration before choosing a name, see here for their current list.

How am I taxed as a Sole Trader?

As a Sole Trader, you would need to complete a self-assessment tax return on an annual basis. The tax year runs from the 6th April to the 5th April, the filing and payment deadline is the 31st January following the end of the tax year.

A Sole Trader would need to keep a record of all income, expenses and assets in order to calculate the profit to declare on the self-assessment, along with any other income received during the tax year. The profit would be at the standard personal tax rates; personal allowance being deducted first and then tax at 20% in the basic rate tax bracket (2020/2021) and 40% in the higher rate tax bracket (2020/2021).

There are two classes of National Insurance that a sole trader would have to pay:

- Class 2 NIC – If a sole trader earns profit in excess of £6,475 (2020/21) during a tax year, then they would need to pay a rate of £3.05 per week (2020/21) through the self-assessment, this equates to £158.60 per annum.

- Class 4 NIC – If the profit for a sole trader is in excess of £8,632 during a tax year, then class 4 NI would be payable, this is broken down into 2 thresholds shown below:

-

- 9% on profits between £8,632 to £50,000

- 2% on profits over £50,000

-

Advantages and Disadvantages of setting up as a Sole Trader

| Advantages | Disadvantages |

| Complete control over how you run and manage your business. You are in charge of decision making. | Unlimited liability – Putting your personal property and possessions at risk |

| Protected by HMRC’s taxpayer confidentiality rules | Lack of employee benefits – As you are working and managing your own business, if you take a sick day or want a 2 week holiday, you won’t get paid. |

| Cheaper costs – No formation fees and cheaper options with Accountancy services | Commitment – To make your business successful, you may have to put in extra-long hours/weeks. |

| Less admin – No company accounts or corporation tax returns to complete for HMRC. No additional paperwork to complete year on year for Companies House | Irregular income – You’ll be paying the running costs of your business, regardless of income. |

| 100% of the profits are taxed | |

| Image – some companies won’t engage with a sole trader |

What is a Partnership?

A partnership is a type of business structure whereby 2 or more people pool together their investment and knowledge to create a business. Similar to a sole trader, each partner would reap the benefits and rewards of the business but also be responsible for liabilities and losses, including those of Limited partners (investors that have Limited Liability and do not get involved in the management of the business).

There are three types of partnerships to consider:

- General Partnership – All partners are involved in the day-to-day decisions and running of the business. The partners are personally responsible for the liabilities of the business and share profits based on their share %.

- Limited Partnership (LP) – Some partners will be general partners as per the above and the other partners will be Limited partners which mean their personal possessions are protected from the company and General Partners actions.

- Limited Liability Partnership (LLP) – All partners are protected by the Limited Liability status, therefore not putting their personal possessions at risk should creditors be seeking payments.

How to set up a Partnership?

To set up a General Partnership, you will need to select a name for the business (the same business naming rules apply as sole traders) and choose a nominated partner. The nominated partner is responsible for sending partnership tax returns to HMRC.

Similar to a sole trader, a partnership must be registered with HMRC by the 5th October in the businesses second tax year, if you don’t you could be fined. Each partner will have to complete their own self-assessment tax return individually in addition to the partnership return.

Setting up a Limited Liability Partnership (LLP) is similar to the process of setting up a Limited Company. The LLP must be registered at Companies House, with accounts submitted on an annual basis. Any changes to the partnership must be notified to Companies House. Nominated members are legally responsible if any of these duties are not carried out.

When setting up an LLP, you may want to seek the advice of an Accountant, Solicitor or Formation Agent to assist you with the formation process.

How am I taxed in a Partnership?

Each partners share of profit in the business is declared on their individual self-assessment tax return, along with any other income received during the tax year. It is always advisable to seek the professional assistance of an Accountant when calculating profits generated and taxes owed to ensure accuracy.

The tax rates, bands and National Insurances due are the same as a sole trader.

Advantages and Disadvantages of setting up a Partnership

| Advantages | Disadvantages |

| A General Partnership has low start-up costs and minimal admin | A General Partnership has unlimited liability |

| Being able to split profits can be tax advantageous | Risk of disagreements between partners |

| General Partnership business affairs are confidential | Partners joining or leaving will require a valuation of the partnership assets which could incur additional costs with the Accountant |

| Sharing the burden of running a business | Unlimited liability and restricted capital can stunt the growth of the business in the future |

What is a Private Limited Company?

What is a Private Limited Company?

A Private Limited Company is the most common form of incorporation in the UK. The company would be formed through Companies House with at least one share and there is no minimal capital requirement. The company is effectively owned by its shareholders.

A Private Limited Company is a separate legal entity to its shareholders and Directors, this means that personal assets are not at risk as the risk is limited to their investment. Liability would only be imposed on the Director in the event of fraudulent or wrongful trading.

How to set up a Private Limited Company?

Firstly you would need to choose a company name that does not already exist; you need to be mindful that your new company name does not include sensitive or offensive words or expressions.

The company would need to be registered with Companies House in the country the company is based; this can be done online through an online formation agent or through an Accountant. On completion of the registration, you will receive an Incorporation Certificate, Memorandum of Articles and Share Certificate. The cost of a formation can range from £10 to £100, depending on how quickly you need the company set up.

How is a Private Limited Company taxed?

The Limited Company will incur corporation tax on an annual basis; this is 19% of profits (2020/21) and paid to HMRC within 9 months of the company yearend (or 21 months from the incorporation date if a new company) from the business bank account. Profit is calculated based on company income less allowable company expenses.

There are a variety of taxes that a Limited Company could register for including the following:

- VAT – A company should register for VAT if the turnover exceeds £85,000 (2020/21) in a 12-month rolling period. The amount payable is dependent on the scheme that your company signs up to; all of these options should be discussed with an Accountant.

- PAYE – If the business has employees that they are being paid a salary, then a PAYE scheme will need to be set up. Tax and employee/employer NI will need to pay to be paid to HMRC.

Extracting funds from a Limited Company and the associated taxes

Shareholders can receive dividends from a Limited Company, this is a distribution made out of available profits in the company. A Director of a Limited Company is not bound by minimum wage and can, therefore, choose to take a low, tax-efficient salary.

Shareholders and Company Directors will need to complete a self-assessment tax return if they receive dividend income in excess £2,000 (2020/21). Company profits do not need to be disclosed on a personal self-assessment return for the Director.

| Up to £2,000 | 0% |

| Basic Rate taxpayers | 7.5% |

| Higher Rate taxpayers | 32.5% |

| Additional Rate taxpayers | 38.1% |

Advantages and Disadvantages of setting up a Private Limited Company

| Advantages | Disadvantages |

| Liability is limited to the investment made in the company | Company formation fees payable |

| A Director is not bound by minimum wage, therefore benefiting from tax advantages | Annual accounts and tax returns that need submitting to HMRC and Companies House – An Accountant can alleviate this stress |

| Improved reputation and credibility | Accounts are published on Companies House which is available to the public |

| Your company name cannot be used by anyone else | |

| Significant tax advantages to contributing to a pension | |

| Allowable expense that can be claimed through the business to reduce corporation tax | |

| There is an element of control over when profits are distributed which can bring tax efficiencies |

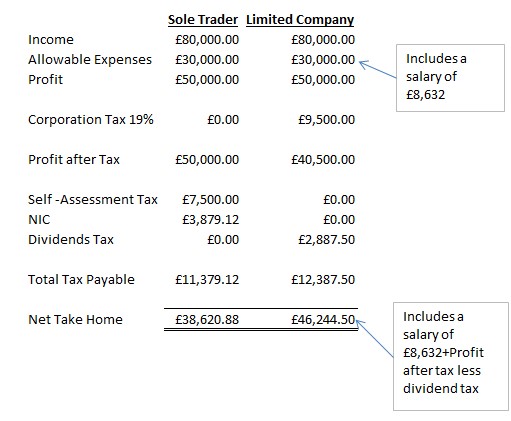

Sole Trader vs Private Limited Company tax comparison

What is a Public Limited Company?

A Public Limited Company is registered under the Companies Act (1980). A listed public limited company can buy and sell shares on the stock exchange. An unlisted company is not listed on the stock exchange and may choose voluntarily not to be listed or it may be because it does not qualify to be listed. Each stock exchange has its own listing requirements that must be met.

How to set up a Public Limited Company?

When setting up a Public Limited Company, firstly a company name needs to be chosen that has not already been taken and is free from offensive and sensitive expressions and words. The application to form a company can be done online through a Formation Agent or Accountant.

Before you can consider your business a PLC, you must register for a trading certificate using the application form SH50 with Companies House.

A minimum of £50,000 share capital is required along with two Directors and a qualified Company Secretary to set up a Public Limited Company. At least a quarter of the share (£12,500) must be paid upon startup.

If you have met the standards required, Companies House will issue the company a trading certificate.

How am I taxed in a Public Limited Company?

A Public Limited Company and Directors are taxed in the same way as a Private Limited Company.

Advantages and Disadvantages of setting up a Public Limited Company

| Advantages | Disadvantages |

| Being able to raise capital by issuing public shares | More regulation to follow |

| Shareholders are able to sell their shares or buy more | Full transparency required for shareholders and investors |

| Greater credibility and professionalism | Accounts must be audited on an annual basis by a qualified auditor which will incur additional costs |

What is the best option for me?

| Private Ltd is best for you if: | Sole Trader is best for you if: | Partnership is best for you if: | PLC is best for you if: |

| You earn more than £16 an hour | Earn lower day rates | There are two of you going into business | There are two Directors and a qualified Company Secretary available to start the business |

| You want to be protected by Limited Liability | Working in this capacity for a short period | You want to share the burden and costs with a Partner | There is a minimum of £50,000 capital of which a quarter is paid up |

| Happy with a bit of extra Admin | Don’t want the extra responsibilities of running a Limited Company | You both don’t want the additional responsibility of running a Limited Company | You are looking to get investors to inject capital into the business |

More on different business structures and limited company taxes to be aware of.

Follow Company Bug